Fellow shareholders,

Atlassian’s mission to unleash the potential of every team advances ever onward, and Q1 was another momentous quarter of executing against our long-term initiatives. We announced a new subscription offering, launched a product into general availability, and held our first large-scale customer event focused on a single market, which got rave reviews from attendees. That said, companies in nearly every industry are facing headwinds, and we’re beginning to see the impact on our business.

In the spirit of our “Open company, no bullshit” value ![]() , let’s start with the topic that’s top of mind for shareholders: macroeconomic impacts.

, let’s start with the topic that’s top of mind for shareholders: macroeconomic impacts.

- Last quarter, we shared that we saw a decrease in the rate of Free instances converting to paid plans. That trend became more pronounced in Q1.

- This quarter, we started to see a slowing in the rate of paid user growth from existing customers.

To be clear, we’re not seeing any changes in our competitive position or in the inherent demand for our products. Looking across our customer base of 249,000+, there has been no overall decrease in usage or change in churn. The above two trends are the result of companies tightening their belts and slowing their pace of hiring. In other words, Atlassian is not immune to broader macro impacts. Our outlook assumes these trends will persist, but we’ll monitor, respond, and keep you updated accordingly.

Turbulent markets provide an opportunity to shake up the leaderboards, and we are poised to play offense in this environment. Buoyed by the secular tailwinds of digital and cultural transformation, Atlassian is incredibly well-positioned to capture additional share in each of our three massive markets – agile/DevOps, IT service management, and work management – and we’re working to do just that. In particular, we have huge opportunities in cloud migrations, serving enterprises, and ITSM – areas where we’ve already seen significant momentum and strong ROI. In the past year, migrations and enterprise deals in the cloud were both up more than 2x, and Jira Service Management added 10k customers.

We will focus our investments on strengthening our market position and scooping up top-tier talent in this environment. But we will balance these investments with the growth of our business and be responsive to macroeconomic conditions. So while we’re lowering our revenue outlook for FY23 based on macroeconomic headwinds, we are maintaining our mid-teens % operating margin outlook for the year. (For further detail, see the Fiscal 2023 Outlook section below.)

Despite the near-term instability in the world around us, we remain certain about the incredible long-term opportunities in front of Atlassian and our ability to capitalize on them. We’ve talked about having a line of sight to $10B in annual revenue. This hasn’t changed.

We have the right products, the right leaders, and the right strategies in place to come out of this downturn in an even stronger position. 💪🏽 When obstacles emerge along the way, we’ll navigate around them as we always have: with vigilance, pragmatism, and agility.

Cloud update: migrations and innovations continue, rain or shine

Migrations from Server and Data Center keep on rolling like thunder. For enterprise customers, the shift to the cloud is all about reclaiming more capacity for innovation and creating customer value as it frees their admins from managing backups and installing new upgrades. In fact, UK-based cybersecurity firm Sophos was able to move engineers off of routine admin work and onto value-driven projects after migrating. 🤘🏾

With the end of support for Server products coming up in February 2024, we’re putting in the hard yakka ![]() removing blockers and smoothing the way to the cloud. With the help of our recent and upcoming hires in R&D, we continue to improve speed, increase the scale of our offerings, and introduce additional capabilities like data access control via API token and enhanced support for HIPAA compliance.

removing blockers and smoothing the way to the cloud. With the help of our recent and upcoming hires in R&D, we continue to improve speed, increase the scale of our offerings, and introduce additional capabilities like data access control via API token and enhanced support for HIPAA compliance.

By migrating to Atlassian’s cloud, we moved away from being pure support to focusing on process enablement and adding value back to the business.

– Daniel Cave, Senior Infrastructure Engineer at Sophos

Our Data Center business continues to benefit from a segment of Server customers who are choosing Data Center as a stepping-stone on their way to our Cloud products. We’ll continue to develop our Data Center offerings even as we focus the lion’s share of our investments in the cloud. We’ve seen this pattern play out over the years, so we know it’s a matter of when (not if) these customers arrive in the cloud.

To that end, we’re delighted to share two new reasons for customers to get excited about Cloud.

Atlassian Analytics begins delivering insights to customers

We celebrated an exciting milestone in Q1 when Atlassian Analytics graduated into open beta for customers of Jira Software and Jira Service Management’s Enterprise edition. ![]() Atlassian Analytics gives users countless ways to visualize data from their Atlassian products and integrated 3rd-party sources, stored in the underlying Atlassian Data Lake. The ability to glean holistic insights into how work gets done across teams is a powerful new capability that will accelerate our migration pipeline and facilitate upsell to Cloud Enterprise editions.

Atlassian Analytics gives users countless ways to visualize data from their Atlassian products and integrated 3rd-party sources, stored in the underlying Atlassian Data Lake. The ability to glean holistic insights into how work gets done across teams is a powerful new capability that will accelerate our migration pipeline and facilitate upsell to Cloud Enterprise editions.

Names like Paypal, DISH Network, and Yum! Brands are already participating in Atlassian Analytics’ beta program – with more signing up every week. ![]() We’re keen to consult with our beta customers over the coming months and incorporate their feedback into the product. A general availability launch is planned for later this fiscal year.

We’re keen to consult with our beta customers over the coming months and incorporate their feedback into the product. A general availability launch is planned for later this fiscal year.

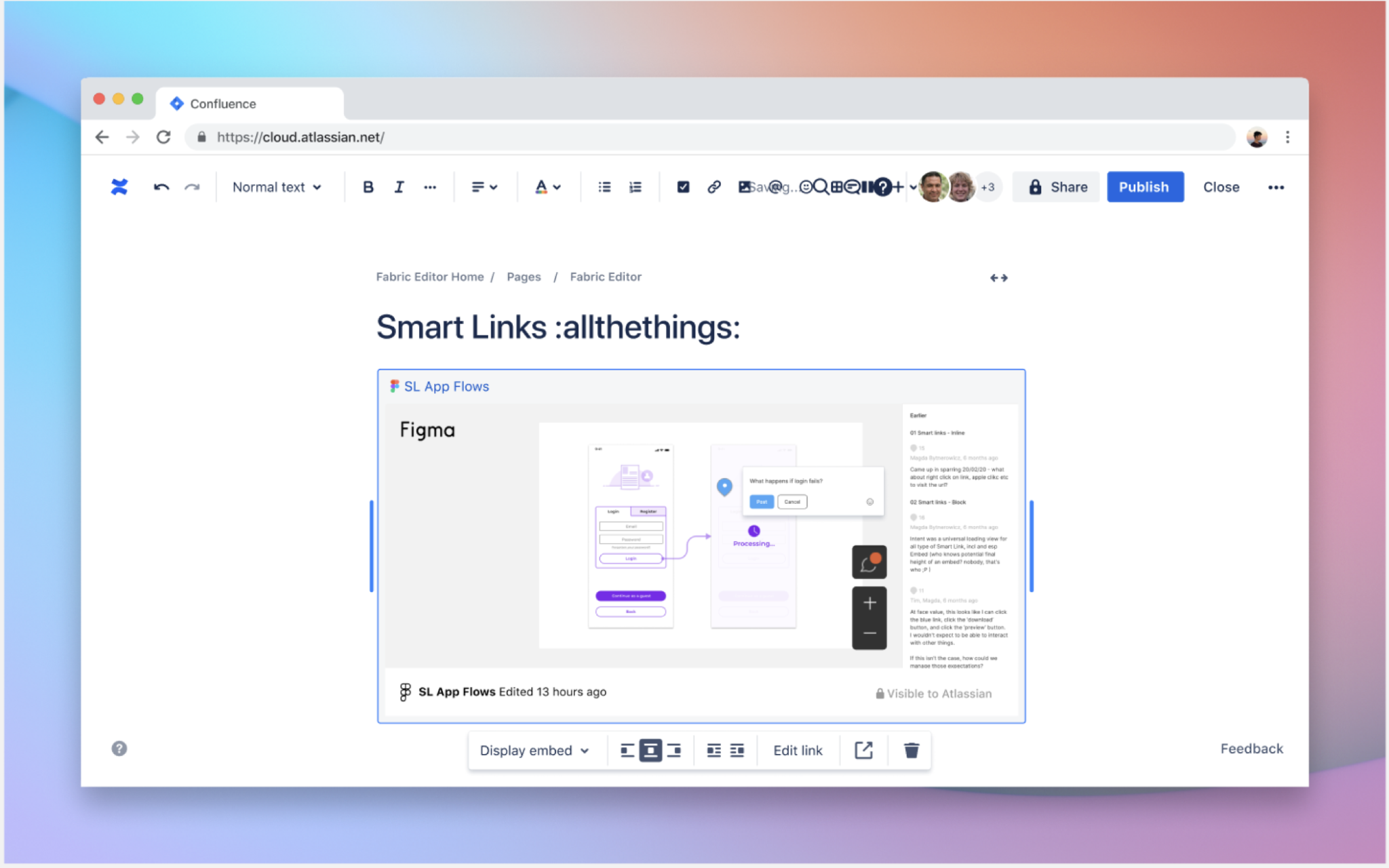

Smart Links make the app explosion less taxing

In a world where knowledge workers flip between applications a staggering 1,200 times a day on average, the “toggle tax” is real. Researchers estimate that the time it takes to reorient oneself after each switch adds up to roughly four hours every week – nearly 10% of their time on the job! That’s why we built Smart Links: a great example of how our platform investments ease customers’ pain points today and into the future (because the Cambrian explosion of apps isn’t likely to fizzle out any time soon).

Smart Links allow customers to find, view, and edit work items across products. Whether it’s a designer embedding a Figma file in a Jira Software issue or a marketer changing the status on an Atlas project without leaving the Confluence page they’re working on, teams get better visibility across the organization and easier access to work regardless of where it happens.

Smart Links are rooted in our principle of helping teams work differently, together. They’re available today in Atlas, Confluence, Trello, Bitbucket, Jira Software, Jira Service Management, and Jira Work Management, where users can embed content from 40+ 3rd-party partners like Google, Microsoft, Miro, Loom, Figma, and Salesforce. It’s one more way our cloud platform’s extensibility brings more value to customers, faster than ever.

Market deep-dive: work management

Every team has work that complements their craft such as planning, tracking, providing updates, and making decisions. So when we look at the massive work management market comprising an estimated 2.2 million companies (those with more than 10 knowledge workers), we see virtually endless opportunities for Atlassian products like Confluence, Jira Work Management, Trello, and Atlas.

Today, teams at over 150,000 organizations worldwide use Atlassian’s work management products. Whereas Jira Software traditionally was the product we’d land with, customers are increasingly coming to Atlassian because of Trello and Confluence as well. And last month, we gave companies one more reason to look our way: Atlas has graduated into general availability. ![]()

Atlas launches into general availability!

Atlas is the new company-wide teamwork directory customers use to connect the dots between people, projects, objectives, and updates – now available to all Cloud customers. Teams register their “big rock” goals in Atlas, as well as the projects and people contributing to them, giving leaders (or anyone else interested) an easy way to keep tabs on the company’s most important objectives.

Since its introduction, customers in Atlas’ early access program have benefited from new features, including:

- Privacy controls – Atlas now supports private projects, which lets users restrict viewing and editing to specific individuals and teams.

- OKR scoring – Ideal for teams that use the Objectives and Key Results framework, goal scoring allows users to assign a projected score based on how confident they are that the team will meet a goal by the target date.

- Kudos! – Recognizing great work with a “kudos” e-card sent to their Atlas feed is a simple, fun, and personal way to thank peers who go above and beyond.

We’re grateful to our early access program customers who helped us refine Atlas’ feature set in preparation for the general availability launch. ![]() Teams of up to 35,000 can use basic Atlas features free of charge. Teams that need advanced features, additional storage, or 24/7 support can upgrade to our Standard or Premium editions.

Teams of up to 35,000 can use basic Atlas features free of charge. Teams that need advanced features, additional storage, or 24/7 support can upgrade to our Standard or Premium editions.

Introducing Atlassian Together

In September, we announced the launch of Atlassian Together: a single subscription to our entire collection of work management products (Trello, Confluence, Jira Work Management, and Atlas). It also includes Access, our enterprise-grade identity and access management solution.

Atlassian Together brings the idea of “working differently, together” to life. It provides a complete, connected toolset so teams can choose the best tool for their needs while ensuring alignment across the organization.

As a manager, it’s my job to ensure everyone works exactly the way they want to and are thriving…Atlassian gives us a central location to store our knowledge and make it easily accessible to people working in different time zones, working with different personal requirements.

– Deepa Aswani, Director of Content at Salesforce*

In other news…

Our “Team Anywhere” program, which gives employees the option to live and work just about anywhere in any country where we operate, continues to be a massive asset for hiring and retaining the best talent. We now have Atlassians in seven Australian territories, 26 Indian regions, 46 U.S. states (plus the District of Columbia), four E.U. countries, and other countries for a total of 13 countries around the globe.

Last month we launched a new recruiting vehicle – literally. The “AtlassiVan” 🚐 is a branded RV that made its way all around Australia with members of our recruiting team taking applications and interviewing candidates on the spot. Through this campaign, we’re taking advantage of the opportunity to become an even more geographically diverse company, as well as demonstrate Atlassian’s commitment to making distributed teamwork work.

We also just released our annual Sustainability Report, highlighting our strategies and achievements related to climate change, human rights, DEI, and social impact. We are ahead of our goals in reducing emissions directly linked to our operations and are now working with our top suppliers on setting their own targets. Our investment in expanding our DEI team and focus on recruitment partnerships is paying off, with hiring rates increasing for underrepresented groups. And we’re incredibly proud of the impact our amazing Atlassians made this year, contributing over 45,000 hours of volunteer time to non-profits in their communities. 🫶🏽

Unlike Jira issues, sustainability never moves to the “done” column. We’re not yet where we want to be on emissions or equitable representation among our staff, but we’re excited to build on this progress as we believe that understanding the connections between people, customers, communities, and the planet is essential for building a 100-year company.

We enter Q2 with immense gratitude to our customers for continuing to build a vibrant community around Atlassian; to our partners for ensuring customers’ success; and to our global team of 9,800 for staying focused on delivering innovative products that enable our customers to do the best work of their lives.

Here’s to the road ahead, and to unleashing the potential of every team.

-Mike and Scott

the bottom line

- Atlassian is not immune to the broader macroeconomic environment. 1) We continued to see a slower rate of Free instances converting to paid plans; and 2) we started to see a slower rate of growth in paid seats from existing customers as companies slowed their pace of hiring. We’re not seeing any changes in our competitive position or in the inherent demand for our products. Looking across our customer base of 249,000+, there has been no overall decrease in usage or change in churn.

- We remain steadfast in our conviction that we have the right leaders, products, and strategies to play offense and strengthen our market position during this downturn. We will balance our continued investments with the overall growth of our business and responsiveness to the current macroeconomic environment.

- Platform innovations like Atlassian Analytics and Smart Links exemplify the unparalleled value our Cloud products offer, and we continue to deliver innovative ways to help our customers with new offerings like Atlassian Together and Atlas.

Customer highlight reel

As mentioned above, conversions of Free instances to paid products continue to be affected by the macroeconomy. We added 6,550 new customers this quarter, bringing our total to 249,173. Importantly though, the number of teams coming to our site and trying Free editions of our products continues to grow.

Customers: We define the number of customers at the end of any particular period as unique domains that have at least one active and paid product license or subscription, with 2 or more seats, excluding starter licenses/subscriptions

In keeping with historical trends, nearly 99% of new customers chose our Cloud products. Our Free editions serve as a key step in our sales funnel and are an important driver of long-term growth for Atlassian. Although we keep our marketing budget leaner than any of our peers, we’ll continue to iterate on our GTM tactics and make targeted investments that get users into our products with as little friction as possible.

Last month we took another step in our GTM evolution when Accenture expanded their partnership with Atlassian. (Welcome, Accenture! ![]() ) This partnership will strengthen our strategic position with enterprise customers and give them the opportunity to work with a partner they already know and trust.

) This partnership will strengthen our strategic position with enterprise customers and give them the opportunity to work with a partner they already know and trust.

Through our strategic collaboration with Atlassian, we are bringing comprehensive enterprise agility solutions to our clients, which aren’t only critical for the technology organization, but for modernizing the way all teams will work in the future.

– Greg Douglass, Senior Managing Director and Global Lead for Technology Strategy & Advisory at Accenture

Getting face-time with customers, one market at a time

The reviews are in: Atlassian’s first market-specific event was a hit. We gathered with partners and customers like Salesforce, Sprout Social, Hubspot, and DISH Network for an afternoon of product announcements, learning about the latest trends in work management, and networking at the Chase Center in San Francisco. Thousands of attendees joined us virtually through live streams and on-demand content.

For me, the best part was meeting face-to-face with leaders from some of our largest customer organizations. We sat down as a group to discuss their thorniest collaboration challenges, swap ideas, share lessons learned, and take in their feedback on Atlassian’s products and services. We’re honored by their participation and continued trust in Atlassian as a strategic partner for their business.

Looking ahead, we’re thrilled to invite customers and partners to our next event, this time focused on IT service management. We’ll be featuring product demos, a fireside chat with customers, and breakout sessions designed to help IT teams work at high velocity.

I’ll be in London for the event on December 8th and would love to see you there. Whether you join us in person or take advantage of the live streams and on-demand content, I hope you’ll make the most of this opportunity to see how Atlassian is unleashing the potential of IT teams everywhere.

– Cameron

Financial highlights

As a reminder, during Q1, we completed the redomiciliation of Atlassian’s parent company from the United Kingdom to the United States. As a result, we have transitioned our accounting standards for reporting purposes from IFRS to GAAP. The primary financial impacts of this transition are detailed below and in supplemental materials on our Investor Relations site.

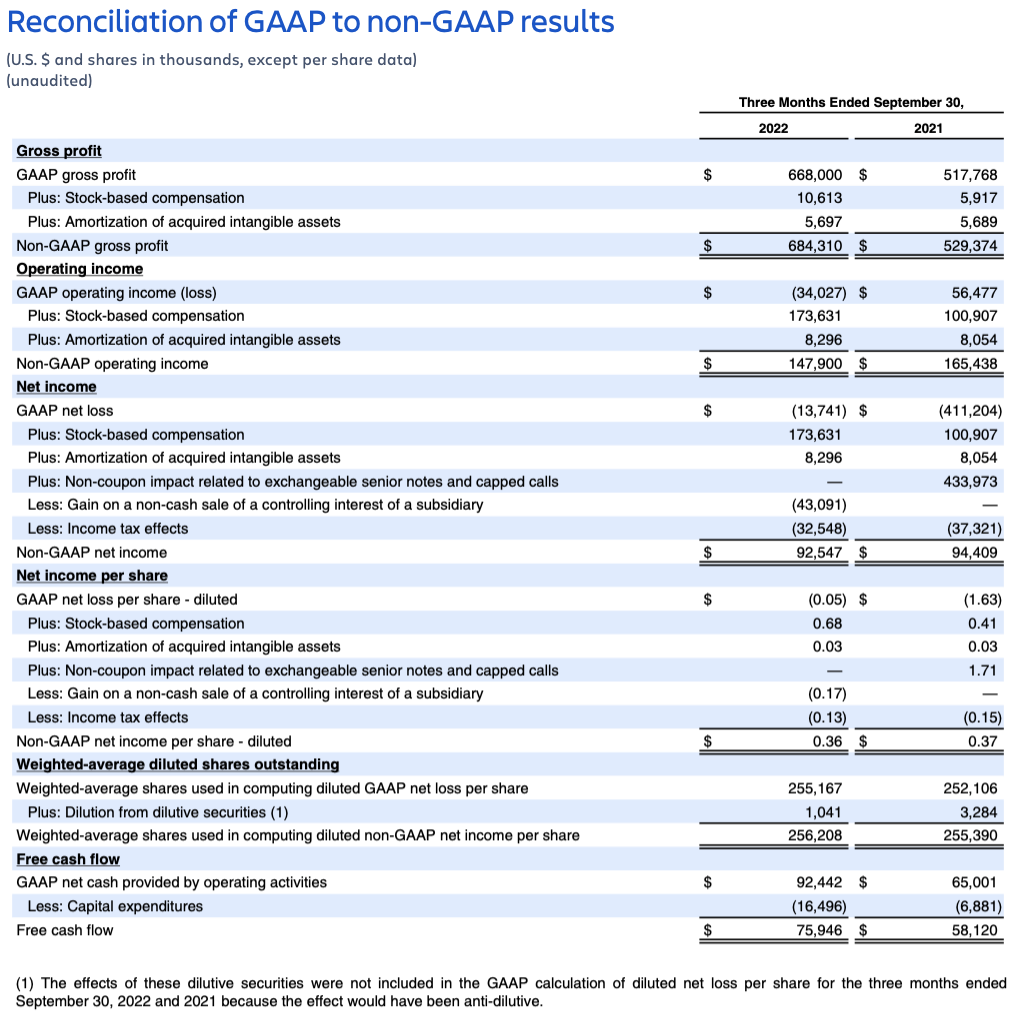

A reconciliation of GAAP to non-GAAP measures is provided within the tables at the end of this letter as well as in our earnings press release, and on our Investor Relations website.

First quarter fiscal year 2023 highlights

We were pleased with our steady financial performance and strong execution in an increasingly challenging macroeconomic environment.

Our cloud migration progress continues to track well with our expectations, and we are making consistent progress toward the long-term goals we laid out at our 2022 Investor Day. Despite the near-term macro headwinds, we remain as excited as ever about the long-term opportunities ahead of us.

Highlights for Q1’23 include:

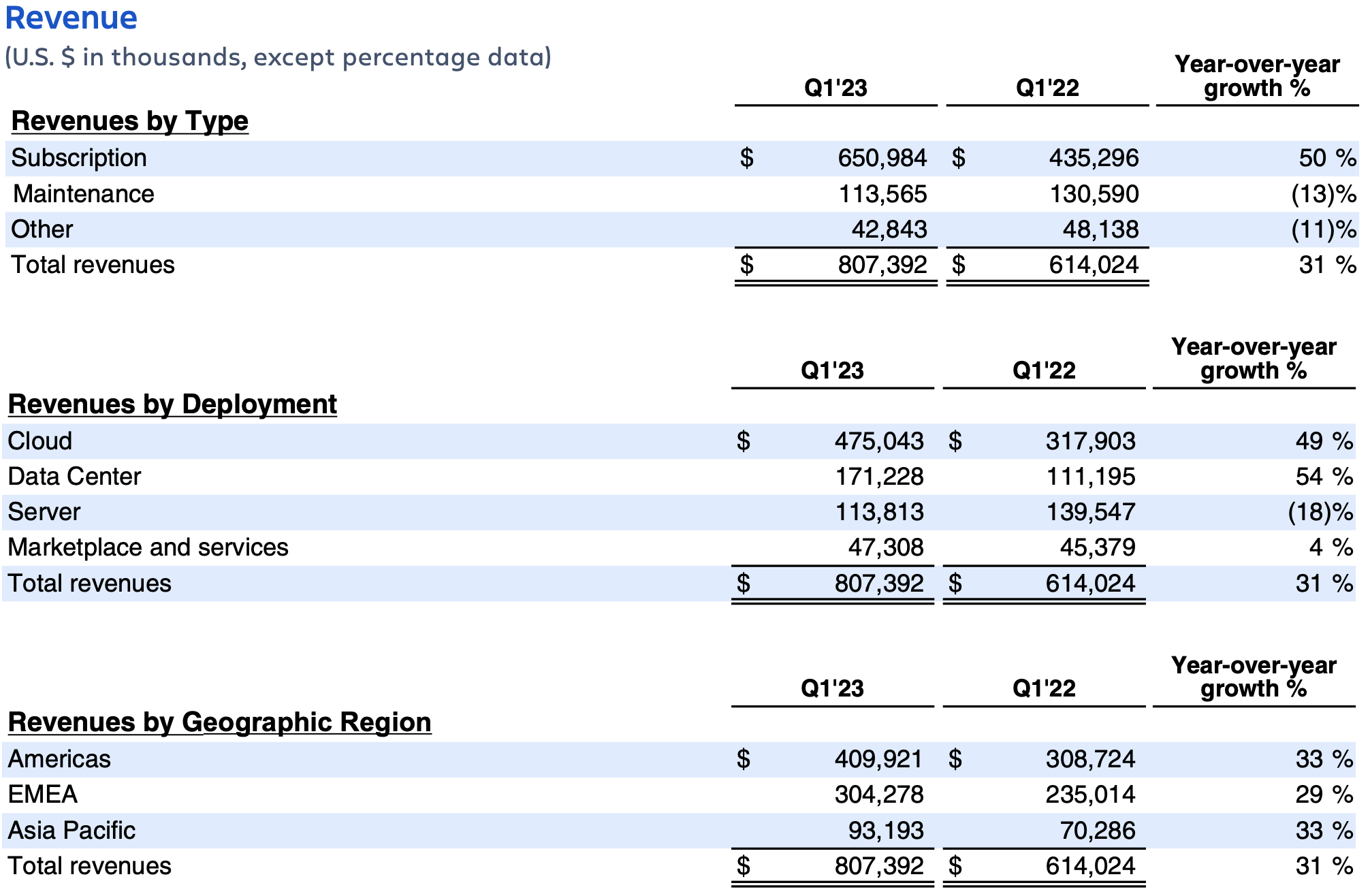

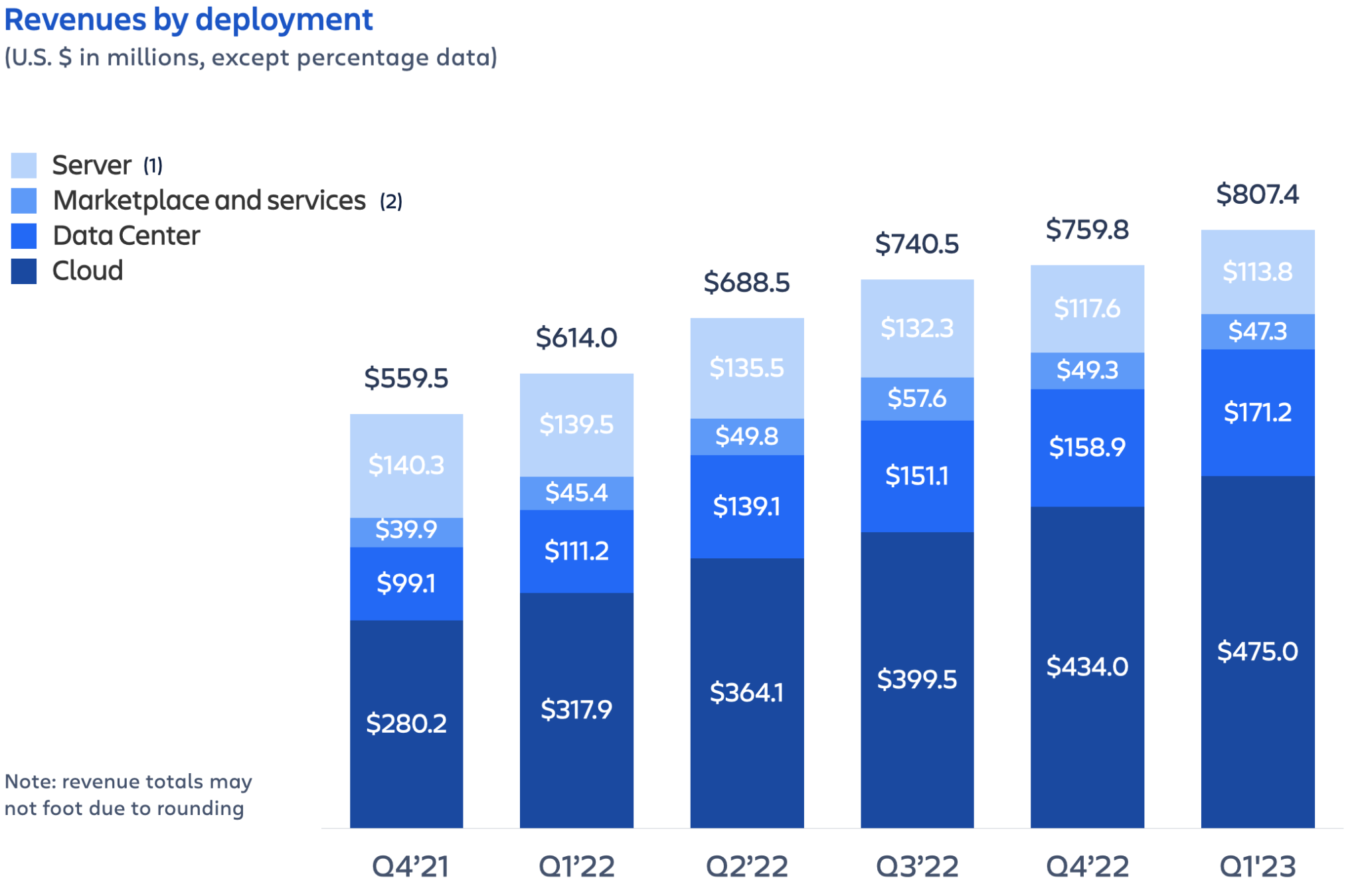

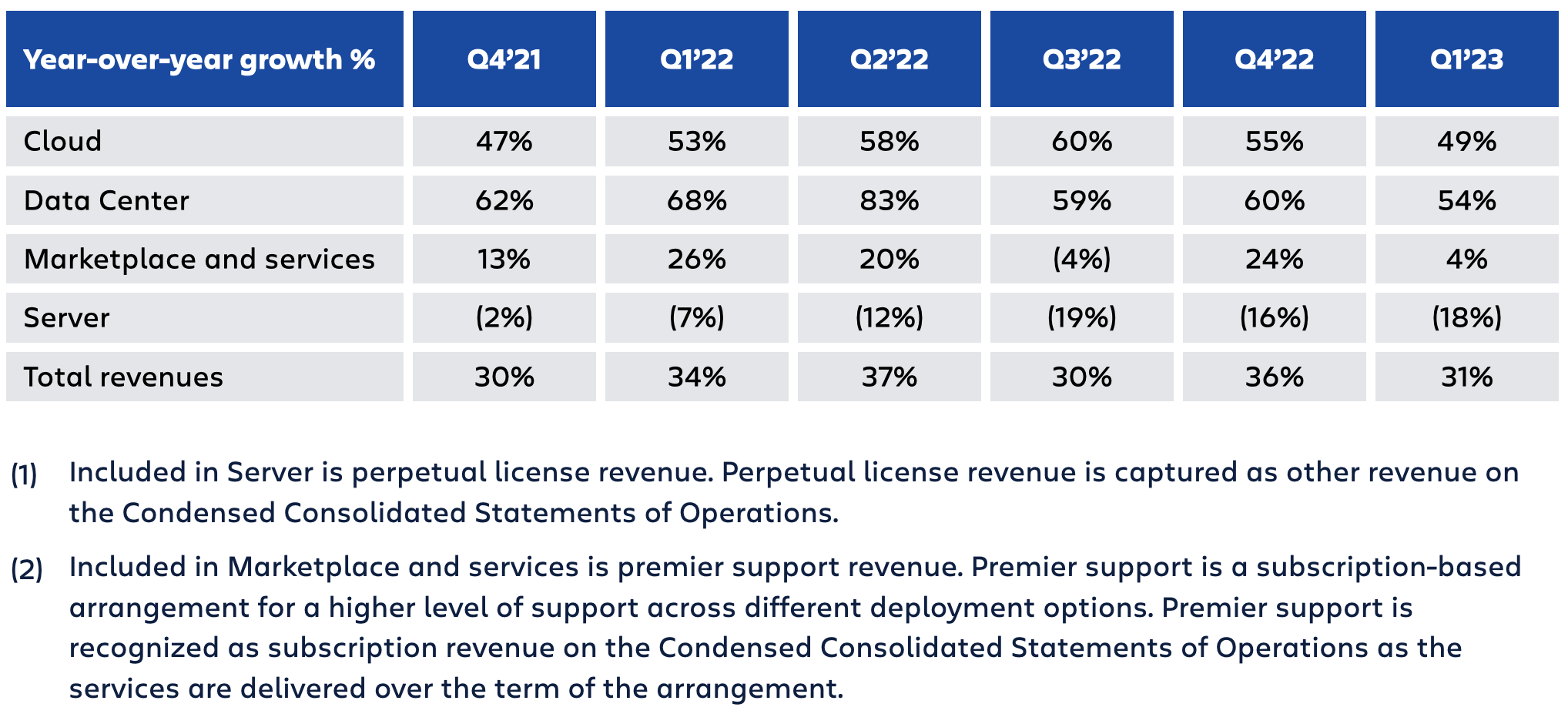

- Subscription revenue grew by 50% year-over-year. Cloud revenue grew by 49% year-over-year and Data Center revenue grew by 54% year-over-year.

- We added 989 net new Atlassians, of which approximately 200 were new college graduates, and ended the quarter with a total headcount of 9,802. We hired across all functions, with the majority in R&D. This is in line with our strategy of adding talented employees to achieve our long-term ambition, and we believe hiring in the current macroeconomic environment is to our advantage.

As discussed by Mike and Scott above, we encountered two primary revenue headwinds during the quarter from changes in the macroeconomic environment: 1) We saw a more pronounced continuation of the trend discussed last quarter, where fewer Free instances converted to paid plans; and 2) we also saw the growth of paid users from existing customers slow in the second half of Q1, largely due to customers slowing their rate of hiring. The impact these headwinds will have on our future revenue growth is detailed in the Fiscal 2023 Outlook section below.

Overall, the underlying fundamentals of our business remain healthy. We continue to focus on hiring great talent, taking share, delivering strong progress in customer cloud migrations and building enterprise capabilities, and investing for long-term success across our three target markets.

As a reminder, we primarily bill our customers in U.S. dollars, and therefore our revenue results in EMEA reflect the impact of the strengthening U.S. dollar.

Net income includes a loss from the mark-to-market accounting of the company’s strategic investment portfolio of $11.6 million in Q1’23 and $31.4 million in Q1’22. These losses resulted in headwinds, on a GAAP and non-GAAP net income per diluted share basis, of $0.05 in Q1’23 and $0.12 in Q1’22.

As a reminder, we experience seasonality in our free cash flow results, with Q1 typically having the lowest free cash flow due to the timing of employee bonus payments. We also saw an impact from the timing of cash tax payments of approximately $17 million that shifted into Q1 from Q2.

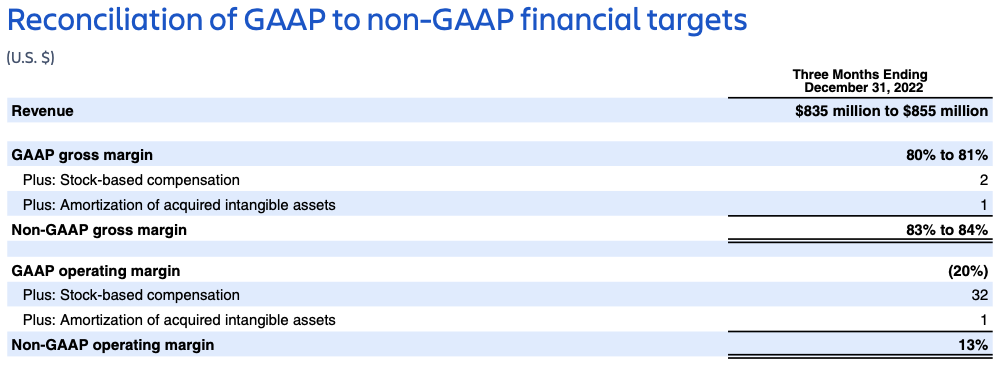

Financial targets

Fiscal 2023 outlook

Our revenue outlook factors in the current macro-related trends we are seeing in our business. We have assumed the current macroeconomic conditions remain unchanged and the trends we saw in Q1 around new customer conversions and paid seat expansion within existing customers persist through the rest of fiscal 2023.

In terms of costs, consistent with our management philosophy and approach, we plan to balance sustained strategic investments across our three core markets and platform to drive long-term growth, with responsiveness to the current environment. We plan to do this through focused operational excellence and execution, prioritized investment decision-making, and disciplined management of our cost structure.

We see the challenging macroeconomic environment as an opportunity to take share and continue to invest in strategic high-growth areas – all with the goal of strengthening our competitive position.

Revenue

In FY23, we expect to see the following trends:

SUBSCRIPTION REVENUE

- Cloud revenue

- Based on the macro headwinds described above, we are lowering our Cloud revenue growth outlook to a range of approximately 40% to 45% year-over-year for FY23.

- We continue to expect approximately 10 points of this growth to be driven by migrations.

- Data Center revenue

- We continue to expect Data Center revenue growth to moderate on a year-over-year basis over the remaining three quarters of FY23, driven by event-driven demand in the prior year resulting from price increases and the reduction of loyalty discounts.

- As a reminder, for Data Center revenue, a portion is recognized up-front in subscription revenue in the period that the subscription begins, while the remainder is recognized ratably over the term of the contract. This may add quarter-to-quarter volatility in Data Center growth rates.

MAINTENANCE REVENUE

- In line with our announced Server end-of-life, we expect maintenance revenue to continue to slowly contract over the course of FY23 to approximately $75 million in Q4’23.

- As a reminder, we will no longer provide maintenance and support for our Server offerings as of February 2024.

OTHER REVENUE

We continue to expect:

- Other revenue to be slightly down relative to FY22.

- Marketplace revenue will be impacted by the ongoing mix shift of third-party app sales from Server and Data Center to Cloud. Sales of third-party Cloud apps have a lower Marketplace take rate relative to Server and Data Center, which is designed to incentivize further Cloud app development. Our focus remains on driving a growth rate on sales of third-party Cloud apps greater than that of our own products.

As a reminder:

- Perpetual license revenue, which is recognized in other revenue, will be $0 in FY23 and total approximately $30 million in FY22.

- Revenue on the sale of third-party Marketplace apps is recognized in the period the product is purchased.

Profitability

We continue to expect the following dynamics to impact our margins in FY23:

- Gross margin will decrease modestly in FY23 due to the continued business mix shift to the cloud and investments we are making to support cloud migrations.

- Operating margin will be in the mid-teens % for FY23, consistent with our previously issued target, despite the macroeconomic headwinds and adjustments to our revenue outlook.

- Free cash flow is expected to be impacted, on a comparative basis, due to the lower operating margin in FY23 versus FY22. Additionally, free cash flow may be impacted as a result of the continued business mix shift to the cloud. Maintenance contracts for our Server products and subscription contracts for our Data Center products are only offered on annual terms, while we offer subscriptions for our Cloud products on both annual and monthly terms. In the short term, the shift to the cloud and the potential mix change in billing terms may create a headwind for free cash flow. Over the long term, as more enterprise customers migrate to the cloud, we expect any such headwind to subside.

Given our transition to GAAP, we are required to recognize unrealized gains and losses on our strategic investments portfolio in other income (expense), which can create quarter-to-quarter volatility and are inherently difficult to forecast. As a result, we will focus our future profitability targets on operating margins and discontinue EPS targets.

Share count

In FY23, we expect an approximately 2% year-over-year increase in diluted share count.

Conversion from IFRS to GAAP

Effective September 30, 2022, we completed the redomiciliation of Atlassian’s parent company from the United Kingdom to the United States. As a result, we transitioned our accounting standards from IFRS to GAAP. We have published materials on our Investor Relations website summarizing the primary impacts of the transition and historical financial results under IFRS and GAAP.

The following areas will be affected:

- Stock-based compensation – GAAP utilizes “straight-line” ratable expense recognition instead of “graded” front-loaded expense recognition under IFRS.

- Leases – Under GAAP, total lease expense is recognized on a straight-line basis over the lease term. Under IFRS, the expense recognition method results in a higher portion of the total lease expense recognized earlier in the lease term.

- Strategic investments – Under GAAP, quarterly mark-to-market fair value movements of equity investments are recorded in other income (expense) on our Condensed Consolidated Statements of Operations, while under IFRS, it is recognized in other comprehensive income (loss), a component of equity, on the Statement of Financial Position. This change introduces quarterly fluctuations on our Condensed Consolidated Statements of Operations.

- Exchangeable senior notes – The amortization of the debt discount and issuance costs relating to our exchangeable senior notes, which were fully settled in Q2’22, follow different timing recognition rules under GAAP. This difference resulted in a portion of amortization shifting from FY21 to FY22.

- Reclassifications –

- Under GAAP, we will characterize certain cash interest payments on financing arrangements as operating cash flows, while IFRS allowed for these to be classified as financing cash flows. This difference impacts cash flow from operations and free cash flow.

- Under GAAP, implied interest related to leases is recognized in cost of revenues and operating expenses on the Condensed Consolidated Statements of Operations instead of in interest expense as it is under IFRS. This difference increases cost of revenues and operating expenses and decreases non-operating expenses.

Forward-looking statements

This shareholder letter contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, which statements involve substantial risks and uncertainties. In some cases, you can identify these statements by forward-looking words such as “may,” “will,” “expect,” “believe,” “anticipate,” “intend,” “could,” “should,” “estimate,” or “continue,” and similar expressions or variations, but these words are not the exclusive means for identifying such statements. All statements other than statements of historical fact could be deemed forward looking, including risks and uncertainties related to statements about our products, customers, partnerships, sustainability initiatives, macroeconomic growth, anticipated growth, outlook, technology and other key strategic areas, and our financial targets such as revenue and GAAP and non-GAAP financial measures including gross margin and operating margin.

We undertake no obligation to update any forward-looking statements made in this shareholder letter to reflect events or circumstances after the date of this shareholder letter or to reflect new information or the occurrence of unanticipated events, except as required by law.

The achievement or success of the matters covered by such forward-looking statements involves known and unknown risks, uncertainties and assumptions. If any such risks or uncertainties materialize or if any of the assumptions prove incorrect, our results could differ materially from the results expressed or implied by the forward-looking statements we make. You should not rely upon forward-looking statements as predictions of future events. Forward-looking statements represent our management’s beliefs and assumptions only as of the date such statements are made.

Further information on these and other factors that could affect our financial results is included in filings we make with the Securities and Exchange Commission (the “SEC”) from time to time, including the section titled “Risk Factors” in our most recently filed Forms 20-F and 6-K (reporting our quarterly results), as well as Forms 10-K and 10-Q. These documents are available on the SEC Filings section of the Investor Relations section of our website at: https://investors.atlassian.com.

About non-GAAP financial measures

In addition to the measures presented in our condensed consolidated financial statements, we regularly review other measures that are not presented in accordance with GAAP, defined as non-GAAP financial measures by the SEC, to evaluate our business, measure our performance, identify trends, prepare financial forecasts and make strategic decisions. The key measures we consider are non-GAAP gross profit, non-GAAP operating income, non-GAAP net income, non-GAAP net income per diluted share and free cash flow (collectively, the “Non-GAAP Financial Measures”). These Non-GAAP Financial Measures, which may be different from similarly titled non-GAAP measures used by other companies, provide supplemental information regarding our operating performance on a non-GAAP basis that excludes certain gains, losses and charges of a non-cash nature or that occur relatively infrequently and/or that management considers to be unrelated to our core operations. Management believes that tracking and presenting these Non-GAAP Financial Measures provides management, our board of directors, investors and the analyst community with the ability to better evaluate matters such as: our ongoing core operations, including comparisons between periods and against other companies in our industry; our ability to generate cash to service our debt and fund our operations; and the underlying business trends that are affecting our performance.

Our Non-GAAP Financial Measures include:

- Non-GAAP gross profit. Excludes expenses related to stock-based compensation and amortization of acquired intangible assets.

- Non-GAAP operating income. Excludes expenses related to stock-based compensation and amortization of acquired intangible assets.

- Non-GAAP net income and non-GAAP net income per diluted share. Excludes expenses related to stock-based compensation, amortization of acquired intangible assets, non-coupon impact related to exchangeable senior notes and capped calls, gain on a non-cash sale of a controlling interest of a subsidiary and the related income tax effects on these items.

- Free cash flow. Free cash flow is defined as net cash provided by operating activities less capital expenditures, which consists of purchases of property and equipment.

We understand that although these Non-GAAP Financial Measures are frequently used by investors and the analyst community in their evaluation of our financial performance, these measures have limitations as analytical tools, and you should not consider them in isolation or as substitutes for analysis of our results as reported under GAAP. We compensate for such limitations by reconciling these Non-GAAP Financial Measures to the most comparable GAAP financial measures. We encourage you to review the tables in this shareholder letter titled “Reconciliation of GAAP to Non-GAAP Results” and “Reconciliation of GAAP to Non-GAAP Financial Targets” that present such reconciliations.

About Atlassian

Atlassian unleashes the potential of every team. Our agile & DevOps, IT service management and work management software helps teams organize, discuss, and complete shared work. The majority of the Fortune 500 and over 240,000 companies of all sizes worldwide – including NASA, Kiva, Deutsche Bank, and Salesforce – rely on our solutions to help their teams work better together and deliver quality results on time. Learn more about our products, including Jira Software, Confluence, Jira Service Management, Trello, Bitbucket, and Jira Align at https://atlassian.com.

Investor relations contact: Martin Lam, IR@atlassian.com

Media contact: M-C Maple, press@atlassian.com

*Source: video shown at Atlassian Presents: Work Life in September, 2022.